Margin Velocity Economics

A Diagnostic Framework for CPG Brand Growth and Acquisition Value

Manoli Kulutbanis · Founder, UpScalability LLC · Author, Pricing Power is Brand Power

Working paper · May 2026 · Version 6

Prepared for the consideration of VCs, PEs and Strategics

What acquirers are paying for

Acquirers do not pay premium multiples for revenue. They pay them for the structural conditions that allow revenue to compound under their ownership without consuming the unit economics that make compounding worthwhile. The shorthand is that acquirers pay premiums for brands that are Easy to Grow.

A brand is Easy to Grow when it is simultaneously Easy to Buy from the consumer's standpoint — the consumer-franchise condition — and Easy to Fund from the brand owner's standpoint — the unit-economics condition.

When both hold, growth begets growth. When either fails, the surface-level revenue metric continues for a period — sometimes a long one — before the failure becomes visible in the consolidated reporting that investors actually see.

Two brands post identical revenue growth in the same year. One is structurally healthier than the other by a wide margin, and the strategic acquirers that will eventually consider buying them know it. The framework that follows makes that difference diagnosable before consolidated reporting catches up.

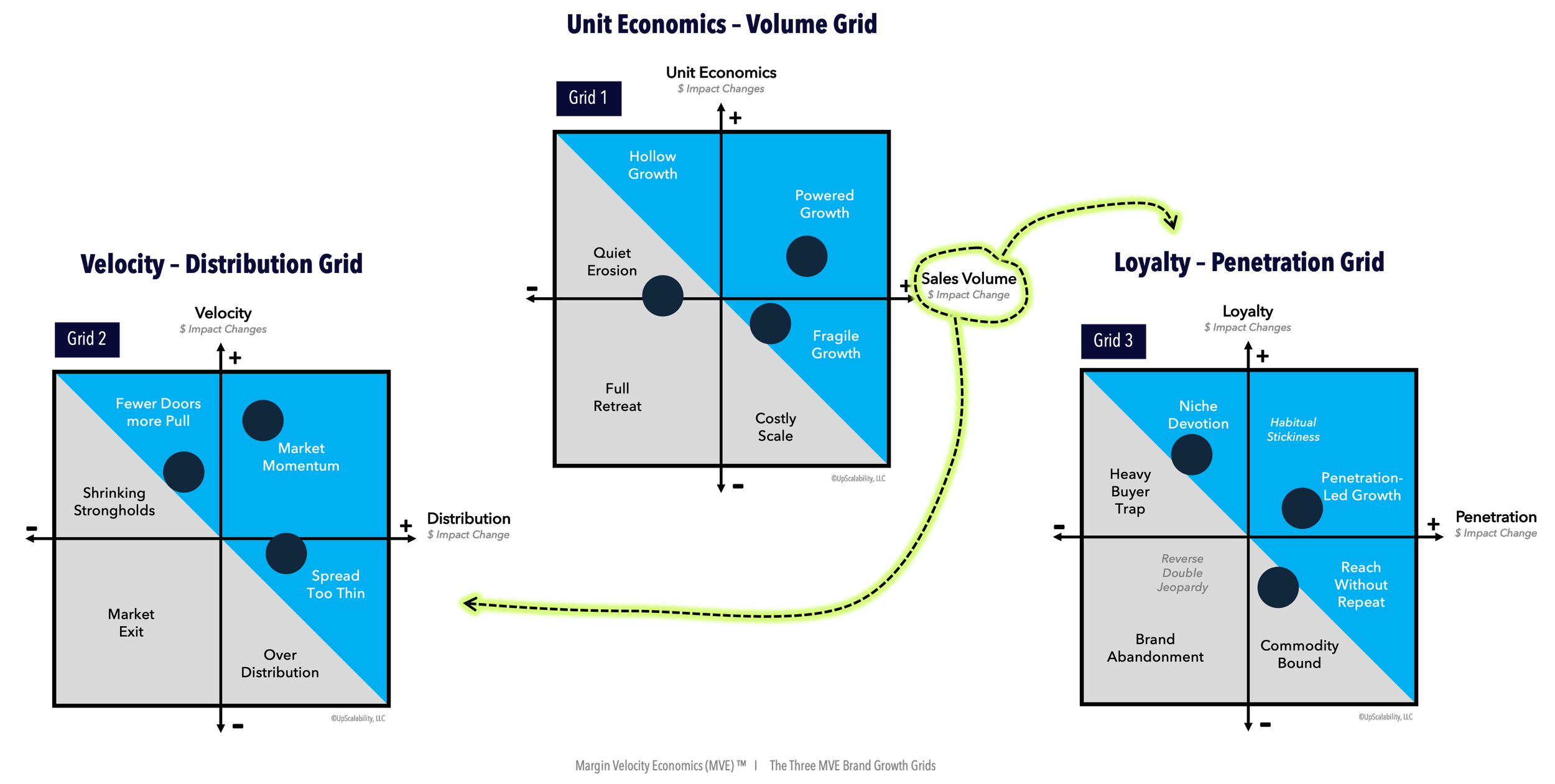

The three grids

MVE consists of three diagnostic grids that decompose the brand's commercial position into observable structural variables.

The three core MVE grids — Unit Economics × Volume, Velocity × Distribution, Loyalty × Penetration.

Grid 1 — Unit Economics × Volume. Separates brands by whether scale is earning its own economics or consuming them. Powered Growth sits at the upper right; Fragile Growth, Costly Scale, Hollow Growth describe the variants of growth that is being purchased rather than earned.

Grid 2 — Velocity × Distribution. Separates brands by whether velocity per door is earning the distribution footprint or whether the footprint is running ahead of consumer pull. Market Momentum sits at the upper right; Spread Too Thin is the inverse condition that recurs across recent acquisition cases.

Grid 3 — Loyalty × Penetration. Separates brands by whether the consumer franchise is broadening or narrowing, and whether stated loyalty metrics reflect a healthy household base or a thinning one. Penetration-Led Growth with sustained Habitual Stickiness sits at the upper right; Heavy Buyer Trap, Niche Devotion, Reach Without Repeat describe the variants where loyalty intensification can mask penetration deterioration.

Together, the three readings produce a structural diagnosis that predicts the brand's revenue trajectory eighteen to twenty-four months ahead of the consolidated quarterly numbers. That predictive lead time is the analytical asset — the difference between underwriting a brand at the price an acquirer wants to pay and underwriting it at the price the structural position justifies.

The framework in application

The full paper carries five contemporary cases (Olipop, Rao's, Liquid Death, Zevia, Kodiak Cakes). Two contrasting reads illustrate the diagnostic value.

Rao's — the Penetration-Led Growth conversion

Sauce household penetration grew at a 37.2% CAGR from 2015 through 2022. Sauce TDPs grew at 23.2% CAGR from 367 to 1,282 over the same window; sauce velocity per million dollars of all-commodity volume grew at 23.6% CAGR from $34 to $121.

The simultaneous compounding of penetration, distribution, and velocity is the structural signature of Penetration-Led Growth.

Campbell's acquired Sovos in August 2023 at a $2.7 billion enterprise value (19.8x adjusted EBITDA pre-synergies). By March 2026, Rao's annual sales had crossed one billion dollars, with consumption growing 14.5% year-over-year.

The framework reading was diagnosable from public data well before the acquisition outcome confirmed it.

Zevia — the counter-clockwise slide into Heavy Buyer Trap

Contribution profit per equivalized case grew from $1.27 in Q4 2023 to $3.60 in Q4 2025 — a 183% improvement. The operational team executed. Yet Zevia traded at a $14.00 IPO price in July 2021 and approximately $1.19 in late April 2026 — a 92% decline.

The 2025 10-K substituted a cumulative-cans-sold-to-date framing (2.6 billion cans) for the absolute U.S. household count language used in prior filings, signaling structural penetration plateau without admitting it.

Read on revenue and margin metrics alone, Zevia would look like a turnaround. Read on the Loyalty–Penetration grid, the structural position was unmistakably weakening.

Contribution recovery does not save the equity when the penetration base is contracting.

How the diagnostic gets used

The analytical decomposition underlying the three-grid diagnosis — the six Sales and Marketing Contribution drivers and the two-lens decomposition of volume change — is described in detail at upscalability.com/margin-velocity-economics.

There is also a qualitative MVE Snapshot tool that produces a directional reading across all three grids in roughly fifteen minutes, using informed judgment from an operator, an investor, or an advisory team. A simplified version is available at upscalability.com/mve-snapshot.

The version used in client engagements integrates the Snapshot reading with quantitative validation against financial filings, syndicated retail measurement, and channel-level disclosures — producing the diagnosis at the level of granularity that underwriting, intervention, and exit decisions require.

Download the working paper

Margin Velocity Economics: A Diagnostic Framework for CPG Brand Growth and Acquisition Value · Working Paper, V6 · May 2026.

If you would like to walk a portfolio brand or acquisition target through the framework — or to commission a diagnostic on a target you are evaluating — contact me directly via LinkedIn or via the link below. The full working paper is available on request.

In conversation

Sources and notes

Rao's case data drawn from Sovos Brands Form 10-K (FY 2022), Sovos Q1 and Q3 2023 earnings releases, Campbell Soup Company acquisition announcement (August 7, 2023), Numerator household-panel and Circana retail consumption data, and Risa Cretella interview in Food Dive (March 2026).

Zevia case data drawn from Zevia PBC Form 10-K filings (fiscal years 2022 through 2025), Q4 2023 and Q4 2025 earnings decks, and NYSE: ZVIA price history.

The terms Easy to Buy, Easy to Think Of, Easy to Find, Mental Availability, and Physical Availability originate in the work of Professor Byron Sharp and the Ehrenberg-Bass Institute. The other "Easy to" constructs used here extend that vocabulary into the unit-economics dimensions that determine whether a brand's consumer franchise can also be funded.

The full Notes and Sources section, with twenty-three numbered citations, appears in the working paper available for download above.